Full coverage auto insurance offers peace of mind — but many drivers assume it’s always expensive. The truth? You can get solid protection at a surprisingly low rate if you know how to qualify. Whether you’re insuring a new car, financing a vehicle, or just want more protection, full coverage doesn’t have to break your budget.

In this guide, we’ll show you how to qualify for low-cost full coverage car insurance, what factors affect pricing, and the discounts most drivers miss.

What Is Full Coverage Auto Insurance?

Full coverage typically includes three main components:

- Liability insurance – covers injuries and damage to others

- Collision insurance – covers your car if you hit another vehicle or object

- Comprehensive insurance – covers theft, fire, vandalism, weather, and animal damage

It’s not a legal requirement in most states, but if you lease or finance a car, full coverage is often mandatory.

Factors That Influence Full Coverage Cost

- Driver’s age and experience

- Driving history (accidents, tickets)

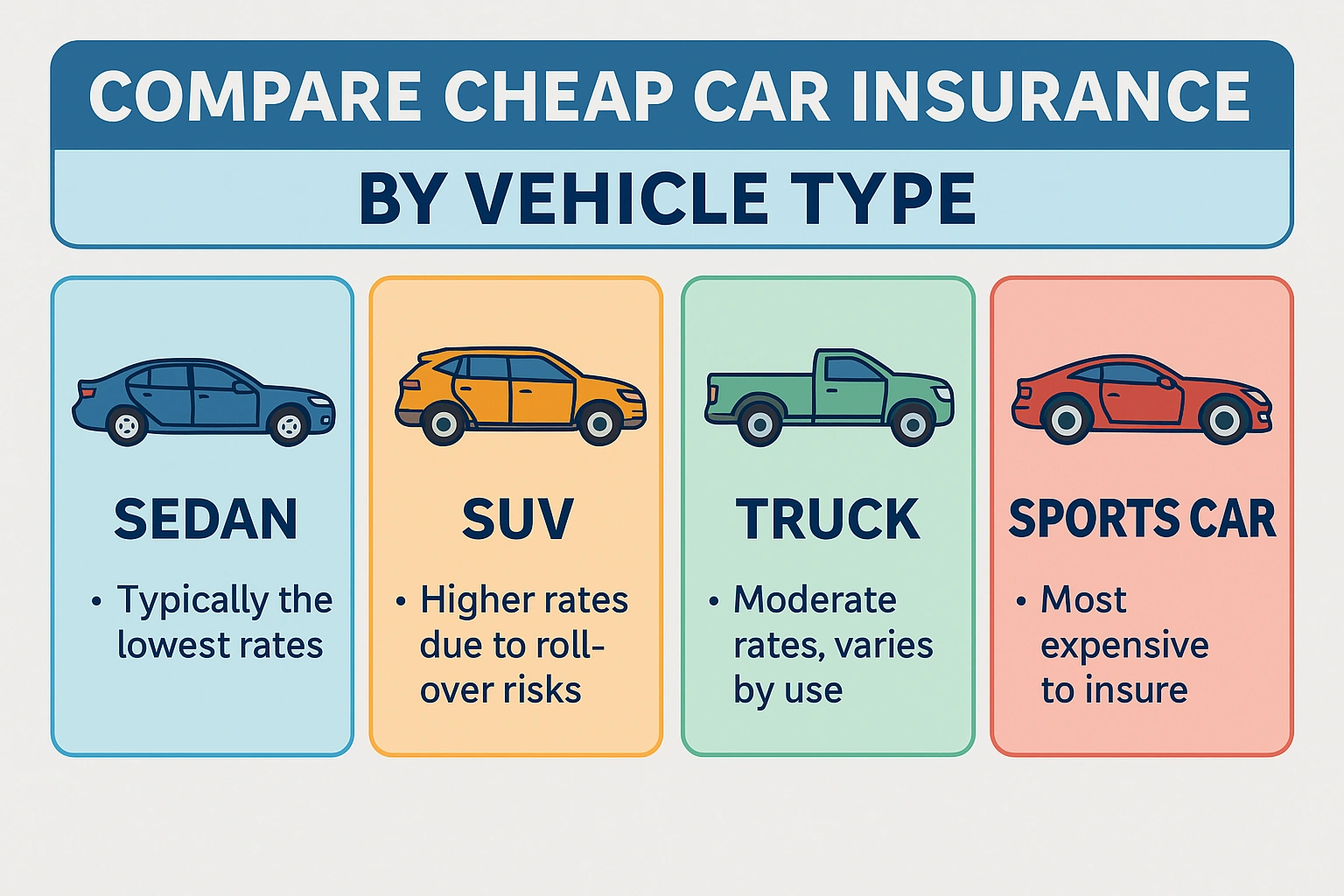

- Vehicle make, model, and age

- Credit score (in most states)

- ZIP code (accident & theft risk)

- Annual mileage

The more risk you present to an insurer, the higher your rate — but that doesn’t mean you can’t lower it.

9 Smart Ways to Qualify for Low-Cost Full Coverage

1. Maintain a Clean Driving Record

Safe drivers pay less. Avoid speeding tickets, DUIs, and at-fault accidents to keep your premiums down.

2. Choose a Safe, Low-Risk Vehicle

Vehicles with high safety ratings and low theft rates cost less to insure. Avoid luxury or high-performance cars if you’re on a budget.

3. Increase Your Deductibles

Raising your collision and comprehensive deductibles from $500 to $1,000 can significantly lower your monthly premium — just be sure you can cover it in case of a claim.

4. Bundle Multiple Policies

Combine auto, home, or renters insurance with the same provider to unlock 10–25% savings.

5. Use Telematics or Safe Driver Apps

Programs like Snapshot®, Drivewise®, and SmartRide® reward good driving with discounts of up to 30%.

6. Ask About Full Coverage Discounts

Don’t assume discounts only apply to basic policies. Ask your insurer if safe driver, loyalty, or student discounts apply to full coverage too.

7. Improve Your Credit Score

In most states, higher credit equals lower insurance rates. Pay bills on time and reduce debt for long-term savings.

8. Re-shop Every 6–12 Months

Rates fluctuate. What was cheapest last year might not be now. Compare quotes regularly to keep your rate competitive.

9. Pay in Full or Set Up Auto-Pay

Most insurers offer small but meaningful discounts for paying upfront or setting up automatic payments.

Full Coverage Discounts and Average Savings

| Discount Type | Eligibility | Average Savings |

|---|---|---|

| Safe Driver Discount | No claims, accidents, or tickets in 3–5 years | 10% – 30% |

| Telematics Program | Enroll in app-based driving monitoring | Up to 30% |

| Multi-Policy Bundle | Combine auto + home/renters/life with same insurer | 10% – 25% |

| Good Credit Score | Credit score above 700 (varies by state) | 5% – 20% |

| Pay-in-Full or Auto Pay | Pay annual premium up front or enroll in autopay | 3% – 10% |

| Anti-Theft or Safety Features | Cars with factory-installed safety/anti-theft tech | 5% – 15% |

| Student or Military Discounts | Full-time students with GPA ≥ 3.0 or active duty service | 5% – 15% |

Best Time to Switch or Upgrade to Full Coverage

- You just financed or leased a new car

- Your car’s value exceeds your current savings

- You’ve improved your credit or driving record

- Your current insurer raised your rates

Final Thoughts

Full coverage insurance doesn’t have to mean full-price premiums. With the right strategies, discounts, and habits, you can protect your car, your finances, and your peace of mind — all at an affordable rate.

Compare quotes today, adjust your coverage smartly, and make full coverage protection work for your budget.